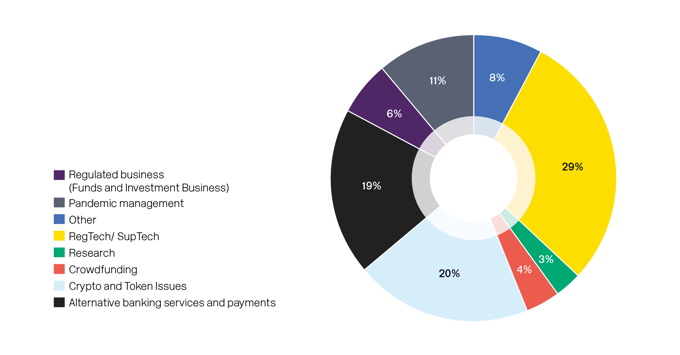

The chart below shows the percentage of enquiries based on broad themes, with the most popular analysed in more detail.

“Other” enquiries relate to businesses that approached us to discuss relevant regulatory touch-points, businesses that asked for assistance with the regulatory process or businesses that wanted to ensure that the JFSC is aware of their solutions, particularly if they are actively marketing to the regulated community.

We do not endorse any product or service, or provide any legal advice.

RegTech

RegTech and supervision technology (SupTech) businesses continued to engage with us and, in almost all cases, wanted to demonstrate their product.

Reasons for this included:

- A new product which they felt may have been of interest to the JFSC’s IT division

- Clients using their service which are also regulated/supervised by the JFSC

- Checking they had not missed any regulatory elements prior to actively marketing their product or service.

These requests spanned across:

- banking

- client on-boarding

- data

- insurance

- intelligence services

- SupTech.

KYC (Know Your Customer) solutions continued to be a key feature for RegTech businesses. We received eight KYC enquiries after publishing our report last July on exploring a smart regulation: shared KYC utility.

Due to the nature of their products and services, these businesses do not typically require authorisation or registration by the JFSC.

Virtual asset activities

We saw a decline in the number of service provider queries as well as businesses looking to issue their own virtual assets in 2020 compared to previous years.

This may be due to changes in market focus as a result of Covid-19. That said, 20% of all enquiries related in some way to virtual asset activities.

These included:

- wallet providers

- trading platforms

- token issuers

- securities issues

- potential new fund launches.

Each business operating in this space is considered on a case-by-case basis by our Registry and Authorisations teams, due to their distinct business models and unique risks.

Alternative banking services and payments

There was a considerable increase in the number of providers engaging with us about offering alternative banking services to Islanders or offering a different type of payment service to the regulated community. We received enquiries from:

- existing EEA-licenced electronic money institutions

- pre-paid card services

- lenders

- technology businesses proposing ‘banking as a service’ integration tools.

A number of sources have cited Covid-19 as a key driver for changing the way B2B2C transactions occur. One report explores how Covid-19 was an accelerator of a series of existing changes, including ‘shifts toward e-commerce, digital payments (including contactless), instant payments, and cash displacement'. Noting this research, and other commentary on this space, it is unsurprising that we saw an increase in the number of enquiries involving alternative banking solutions and payment methods.

Pandemic management

11% of enquiries were from businesses that already hold a licence with us to conduct regulated activities. These businesses were exploring opportunities to use technology during the pandemic to meet regulatory expectations. These included enquiries relating to applying our outsourcing policy, recordkeeping in a digital world, and broader digital transformation initiatives.

Global Financial Innovation Network – Cross-border testing

In 2019, we participated in the GFIN’s cross-border testing pilot, which saw five businesses express their interest in developing their products and services in Jersey.

The application window for 2021 cross-border testing closed on 31 December 2020, and nine firms have expressed an interest in Jersey. We are currently reviewing applications and will form a consensus with other participating regulators.